Robert vt Hoenderdaal/iStock Editorial via Getty Images

The following section was excerpted from This fund letter.

valid basic (BSFFF)

Basic-Fit has been gaining quite a bit lately, especially after it appeared on the Business Breakdown podcast (we promise our research started much earlier than that). The podcast has been released!).

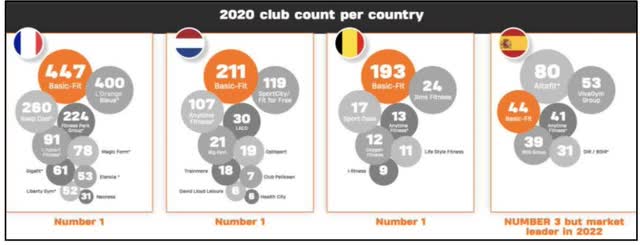

Basic-Fit is Europe’s largest fitness chain with over 1,000 clubs across Europe and over 2 million members, focused on providing a comfortable, low-cost fitness experience. The search for Basic-Fit reminded us of the perfect example for a business beginner, where a single “lemonade stand” generates solid profits that are reinvested to create a chain of lemonade kiosks.

Likewise, the average Basic-Fit Club has an after-tax return on investment of 20%+ (by our calculations), driven by a poor operating model of fewer employees per store, significant equipment discounts due to scale, and the ability to spread market costs over multiple Stores via their own group strategy.

Basic-Fit is run by René Moos, a former professional tennis player, who started HealthCity in the Netherlands in 2004. What was originally a medium to premium gym concept was incorporated into Basic-Fit (via additional mergers and flows) which focused On the low-cost end of the market after the success of Planet Fitness in the US.

The company operates in France, Holland, Belgium, Spain and now Germany. It has a significant advantage over its competitors in most of its markets and is implementing a strong team strategy. This means opening several clubs in a given area within a short period of time, increasing club access for gym goers.

We feel that this increase in access will also increase the penetration of gym goers in Europe which lags far behind its US counterpart (8% vs 20%+). This is demonstrated by real examples of Basic-Fit entering the market and increasing penetration of gym-goers into the group (not only taking a stake but also growing the pie).

When we spoke to the company, one of the big questions we asked was why none of their competitors could copy it — and the company admitted that what they’re doing isn’t rocket science. But after further conversations with the company and other investors, as well as our internal discussion, we came to two conclusions.

First, an aggressive expansion strategy (the goal is to reach more than 3,000 clubs by 2030) requires some special components

- strong execution

- access to capital and

- Aggressive but competent leader.

We feel Basic-Fit has all three.

Second, we feel that her size makes it hard to compete with her.

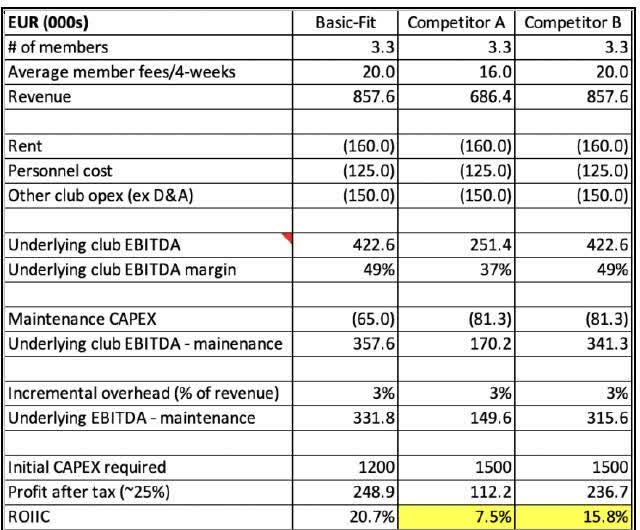

In the chart below, you can see that we are comparing one Basic-Fit club with two hypothetical clubs of competitors, the first (Competitor A) trying to compete on price and the second (Competitor B) trying to completely copy Basic-Fit.

We’re assuming the cost of rent/similar employees/other operations (despite its basic size, Basic-Fit gets rent discounts in certain markets and because of the way its clubs are set up, it can run on skeleton crews). We then build benefits for required upkeep and upfront expenses because, according to industry experts, Basic-Fit has a minimum of 30-40% off mom-and-pop gyms and a 20-25% off off other gamers of the right size.

One can also see that the ROIIC is much lower for both the hypothetical competitors. So even if competitors do show up (which is always a possibility), we doubt they’ll do nearly as well as Basic-Fit.

Now, investing in Basic-Fit involves certain risks. First, the company has about 550 billion euros in net debt on an equity base of 410 billion. Furthermore, we believe the company will need to borrow more over the next three years to achieve its expansion targets of around 250-300 clubs annually. However, we believe that despite the high level of debt, leverage ratios will actually decrease as clubs start to post EBITDA after closings.

Second, a lot of the internal IRR numbers (in the mid 25%) are based on the company’s achievement of 2025 goals for approximately 2,000 clubs and 2030 goals for approximately 3,000 clubs. What we’ve learned over the past few years is that a lot can happen now and then.

Thus, we will scale the situation slowly as the company implements.

Editor’s note: The bulleted summary of this article was selected by searching for the alpha editors.